A detailed update on the continued popularity of regulatory modelling expertise within UK financial services institutions

Introduction (2 min)

We’ve seen regulations within the UK financial services sector develop dramatically in recent times. Shaped by international standards as well as domestic priorities, FS regulations are more abundant, complex, and heavily scrutinised than ever before.

Largely due to major events that have hit financial markets and consumers hard – things like the 2008 financial crash, the COVID-19 pandemic, and the more recent cost-of-living crisis – the need for a boost in financial stability, consumer protection, and keeping up with rapid technological advancements has been heavily highlighted in the past few years.

Regulations have also had to change a lot to keep pace with how financial services themselves have altered. If you think about how much the sector has transformed in the last twenty years, it’s dramatic – from traditional in-branch banking to everyone using desktops and mobile platforms; big shifts in what consumers desire and expect, and how they want to learn about and access financial products; and a constant stream of new products and services that need new or updated rules.

All of this has created a real rollercoaster of demands when it comes to the skills and expertise that financial services businesses need, particularly in their Credit Risk & Analytics teams, to make sure they can handle these fluctuations and see what’s coming down the line.

Right now, one of the biggest trends is the demand for people adept in regulatory modelling. Of course, that’s tied to a lot of what we’ve just talked about. But regulatory modelling has been a key skill for a while now, and the demand is only getting stronger.

As Marcin Lomot, senior Credit Risk & Regulatory expert, says, regulatory modelling has always been there in some shape or form…

“Regulatory modelling has always been there in some shape or form with the financial firms performing periodic regulatory horizon scanning and applying a spectrum of qualitative to quantitative approaches to understand financial, operational, legal and other potential impacts.

It is the recent pace, volume and increased complexity of regulation that may have created greater focus on ‘regulatory modelling’ and helped turned this into what could arguably be perceived as a discipline or profession in its own right; a term has been coined, one could say.”

In this report, MERJE Credit Risk & Analytics recruitment experts Ellie Sykes and Nuhaa Mohamed will be looking at why that is, with some additional insights and perspectives from leading credit risk professionals in the industry today.

Section 1: The latest UK Financial Regulation spotlights and their impact on modelling (3 min)

Exploring the specific recent regulatory changes and areas of increased scrutiny in the UK that are driving the demand for regulatory modelling expertise.

Basel 3.1

Basel 3.1 finalises the Basel III reforms, revising standardised approaches for credit risk, market risk, credit valuation adjustment (CVA), and operational risk to enhance bank resilience and make firms’ capital ratios more consistent and comparable

The Prudential Regulation Authority (PRA), in consultation with HM Treasury, announced in January 2025 that it has decided to delay the implementation of Basel 3.1 in the UK until January 2027. This allows more time for greater clarity to emerge about plans for its implementation in the United States and ensure that the UK aligns with international standards.

Despite the delay, the implementation of Basel 3.1 is a significant undertaking for UK banks and is a key driver of the current demand for regulatory modelling expertise within the financial services sector.

The new rules necessitate substantial changes in how banks calculate their risk-weighted assets (RWAs) and, consequently, the amount of capital they are required to hold. This complexity drives necessity for expertise across several areas:

- interpreting and understanding the regulatory requirements, implementing new methodologies, and updating RWA calculation engines

- building standardised approach calculation capabilities for impact assessment, and potentially adjusting capital planning and business strategies

- gap analysis, capital impact assessment, operating model changes, and informing strategic decisions

- modelling expertise to ensure compliance with the updated requirements and demonstrate the robustness of internal models

- granular data sourcing, data management, and data modelling for ensuring the availability and quality of data for accurate risk calculations

- navigating the transitional period until full implementation also requires careful planning and modelling to understand the evolving capital requirements over time

Ellie, Director of Credit Risk & Analytics recruitment at MERJE, adds,

“Overall, Basel 3.1 introduces an intricate set of regulatory changes that demand significant knowhow in regulatory modelling. Because of this, financial institutions in the UK have been and continue to seek professionals who can interpret these new rules, build and implement compliant models, assess the impact on their businesses, and steer through the implementation process effectively.”

Drawing on his 20+ years contracting in the Credit Risk space, Jamie Hopkins, shared his thoughts,

“Interpretation of the Basel 3.1 regulations is the most demanding area as PRA guidance is not prescriptive and is open to interpretation. To make things more difficult, feedback at PBL mortgage meetings suggested banks had different and sometimes contradictory feedback.

Whilst most banks have submitted Basel 3.1 compliant IRB models to the PRA by now (June 2025), very few have had model approval.

The challenge for larger banks is determining what model changes are required to comply with Basel 3.1, so their work continues to enhance submitted models to comply with PRA requirements.

Smaller banks may have more need for regulatory modellers as they begin their IRB journey to ensure Basel 3.1 compliance.”

Consumer Duty

The Consumer Duty came into force for open products and services on 31 July 2023 with the aim of delivering better outcomes for Financial Services customers. Under the Duty, firms aim to continuously address issues that risk causing consumer harm.

Desired outcomes of the Consumer Duty in a nutshell:

- Give Consumers confidence in retail FS markets with healthy competition, ample support, and high standards of products and services

- Allow vulnerable customers to access outcomes as good as other consumers

- Firms to sell products and services that meet consumers’ needs and offer fair value

- Ensure consumers fully understand the information they’re given to empower them to make considered, timely, and informed decisions

This means embedding the Consumer Duty and Fair Value principles within credit risk frameworks. As such, businesses are enhancing their credit risk teams with professionals who understand affordability, vulnerability, product design, data quality, and monitoring.

Nuhaa, Credit Risk & Analytics senior researcher at MERJE, explains,

“Against a backdrop of economic instability and cost-of-living pressures, embedding these crucial customer-centric considerations into core processes and strategies is vital, and finding and securing the right talent to do so is proving more and more challenging.”

Section 2: Beyond Basel 3.1 and the Consumer Duty (3 min)

After acknowledging the ongoing importance of Basel 3.1 and the Consumer Duty, let’s delve into other areas of regulation that are driving demand.

The Bank of England’s Regulatory Initiatives Grid flags several ongoing and upcoming changes impacting the financial services sector. These initiatives, whilst diverse, collectively contribute to a sustained and growing demand for regulatory modellers and experts, particularly within credit risk functions.

Here’s a summary and analysis of some key initiatives:

The Treasury (with input from the FCA/PSR/CMA) is developing a long-term regulatory framework for Open Banking, aiming to secure existing achievements and unlock future potential.

Impact: This will require modellers to develop and adapt models to incorporate and manage the increased data flows and new business models arising from Open Banking.

Managing Climate Related Risks

The PRA is consulting on the management of climate-related risks to bring the expectations into closer alignment with international standards.

Impact: This will drive new skill development in candidates, as well as the upskilling of existing modellers or hiring of experienced individuals to meet advancements in climate risk regulation.

Managing Climate Related Risks

The PRA is consulting on the management of climate-related risks to bring the expectations into closer alignment with international standards.

Impact: This will drive new skill development in candidates, as well as the upskilling of existing modellers or hiring of experienced individuals to meet advancements in climate risk regulation.

The PRA has published a Supervisory Statement outlining five key principles for effective model risk management.

Impact: This reinforces the need for robust model governance and validation frameworks, increasing the demand for experienced model risk professionals.

Following the Financial Policy Committee (FPC)’s recommendation, the FCA and PRA are consulting on raising the de minimis threshold for mortgage lending.

Impact: Whilst seemingly a minor adjustment, this requires analysis of potential impacts on lending portfolios and risk profiles.

Consultation and Review of the Commercial Credit Data Sharing (CCDS) Scheme

HM Treasury is launching a consultation to review the effectiveness of the CCDS scheme.

Impact: Any changes to data sharing will require adjustments to credit risk models.

HM Treasury is reforming the CCA to modernise regulation of the UK’s non-mortgage consumer lending market.

Impact: This will necessitate changes to credit risk models to comply with the modernised regulatory framework.

Overall Impact on Demand for Regulatory Modellers

These diverse regulatory initiatives are driving a sustained need for skilled regulatory modellers. As such, businesses are looking for Credit Risk & Analytics professionals who can demonstrate strong skills across:

- Developing and validating models: To accurately assess and manage credit risk under new and revised regulations.

- Data Management: To handle the increasing volume and complexity of data required for regulatory reporting and risk assessment.

- Regulatory Interpretation: To understand and implement the nuances of each regulatory change.

- Strategic Planning: To advise firms on the potential impact of regulatory changes on their business models and risk profiles.

Ellie has been recruiting in the Credit Risk & Analytics space for just under 20 years. As such, she has seen the ebbs and flows of the market:

“The regulatory landscape is dynamic yet persistent. There is a continuous need for financial institutions in the UK to invest in skilled regulatory modelling expertise to handle the fluctuations and ensure continued compliance and competitiveness.”

Section 3: The Regulatory Modelling Talent Crunch (2 min)

Addressing the supply side of the equation, examining the scope of the high demand and the challenges firms face in finding qualified regulatory modellers, as well as the challenges faced from a candidate point of view.

According to LinkedIn data, (as of April 2025) there are around 6.2k UK Credit Risk professionals on LinkedIn with IFRS or IRB expertise. This drops to c. 4.8k when looking specifically for modelling experience.

Now take into account that only half (54%) of those professionals are open to new opportunities, and this significantly lowers the talent pool that the whole of the UK has to hire from.

Furthermore, 60% are located in and around London, leaving slim pickings for businesses with regional offices.

Even with the (now waning) flexible working trend, companies often still require employees to visit, or at least be commutable of, an office. With only ~2k experienced candidates to choose from outside of London, it’s no wonder that companies are struggling to recruit regulatory modellers.

All this is before we’ve even considered how to actually get job vacancies in front of these candidates and convince them to click apply.

Nuhaa, who has built a vast network of credit risk professionals over her years of recruiting in the space, knows how difficult it can be to find the right talent:

“With a constant onslaught of LinkedIn posts and hundreds of job vacancies advertised every day, how likely is it that your regulatory modelling job advert is getting in front of the right people? Or that credit risk candidates know to go searching directly on your website because you only advertise jobs there?”

So, how can you improve your hiring strategy to recruit (and retain) regulatory modellers? Ellie and Nuhaa are here to help. Let’s take a look…

3.1: Advice for Clients (6 min)

Advice & Suggestions

Promote your jobs effectively

When we asked our network, we found that 76% of people head to LinkedIn as their first port of call when looking for a job. If you have the resources, capitalising on LinkedIn’s searching functionality and quick-to-market features (like the Open to Work spotlight when searching for candidates) can vastly improve your search success and speed.

This also highlights the importance of advertising roles beyond your company careers site. Posting job adverts on LinkedIn and other job boards significantly increases the chances of your job vacancy being seen by the right people.

As with many business needs, though, whether you are able to do this comes down to resource and budget:

- Do you have the internal availability to sift through hundreds of CVs?

- Do you have the time to spend a minimum of 15 minutes per candidate on the phone, qualifying their skills and experience to confirm whether they’re suitable to interview?

- Do you have the budget to advertise across LinkedIn, Reed, Monster, Indeed, etc. and specialist job boards?

- Do you have the budget to invest in advanced recruitment tools to facilitate deeper candidate search strategies?

The answer to any one of these, if not all of them, is probably no.

That’s where recruitment agencies come in. We already have contracts in place across all major job boards and specialist careers websites. And it’s our bread and butter to spend the 9-5 (or 8:30am-5:30pm in MERJE’s case) filtering through stacks of CVs, making qualifying phone calls, and separating the irrelevant from the star candidates.

Ellie also confirms,

“As recruiters, not only do we have the time and resources to go to market quicker and more effectively, but our specialist nature means we already know what you need. Where your internal TA team may not fully grasp the niche and technical aspects of credit risk and regulatory modelling roles, our decades of experience mean we know them inside out, which streamlines the process substantially.”

Stand out in the employer crowd

You may have heard many people prophesising that salary is the most important factor in a candidate’s job search. Actually, no, it’s flexible working. Maybe career paths are the big priority? Or is it diversity and inclusion?

Opinions on what candidates really look for when choosing their next employer differ widely (although everyone agrees that free fruit and dress down Fridays are past their sell-by date).

Luckily, LinkedIn has data for this too. They’ve asked UK professionals to rank which employer value propositions are most important to them, and these are the top five amongst Credit Risk regulatory modellers:

- Flexible work arrangements (i.e. when and where you work) 54%

- Excellent compensation and benefits 50%

- Opportunities for career growth within the company 40%

- Job security 39%

- Organisational support to balance work and personal life 37%

You can’t argue with information from the horse’s mouth!

Adapting your company culture, benefits, and value proposition to what candidates actually want is a good way to differentiate your business from your competitors.

Be open-minded on location

Interestingly, LinkedIn highlights three “hidden talent locations” – places where the availability of professionals is high relative to hiring demand.

For Credit Risk professionals with IRB or IFRS modelling skills, these untapped talent pools are in Glasgow, Edinburgh, and Leeds (as of April 2025).

With this in mind, maybe it’s worth relaxing your flexible working policy to allow candidates from further afield to apply. Or targeting these areas specifically when searching and advertising your roles.

Is flexible working really THAT important?

The UK’s regulatory modelling professionals have spoken. You can see above that flexible work arrangements are the number one priority for them when considering future employers.

On the recent decrease in flexible working availability, Nuhaa adds,

“While many businesses are pushing the return-to-office agenda, remote and flexible working demands from candidates are not going away. Indeed data shows that searches for remote jobs are 9x higher than pre-pandemic levels. If you’re finding recruitment difficult, reviewing your flexible working policy is a good place to start.”

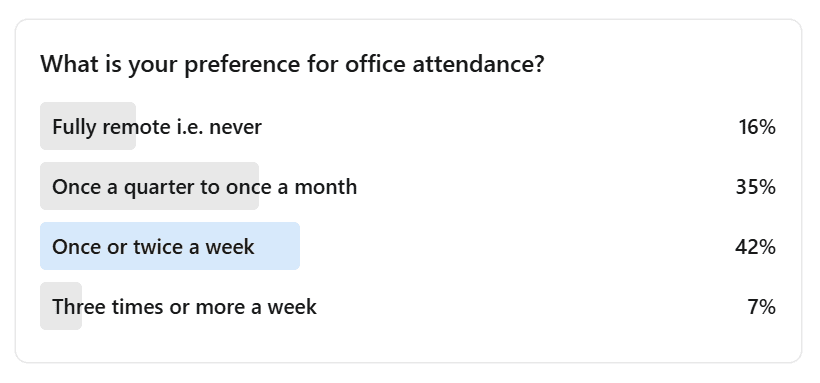

When Ellie Sykes asked her Credit Risk network about their flexible working preferences, the results were resounding.

Just 7% of respondents would want to be in the office 3+ times per week.

This is a stark revelation considering that, as of Q4 2024, ~85% of jobs advertised in the UK were fully onsite roles. While this number is still down from pre-pandemic levels of 96%+, there remains a drastic gap between employer expectations and candidate preferences when it comes to working arrangements.

If employers weren’t already struggling to hire due to limited budgets and niche skill requirements, restricting your talent pool to less than 1 in 10 possible candidates because of your strict office-based working policy makes your hiring projects almost impossible to complete.

On the other side of the equation, this also means that hybrid and remote job adverts – making up just 15% of all opportunities in the UK – are flooded with applications as over 90% of candidates are looking for at least some level of working from home flexibility.

How will this tug-of-war between employer demands and candidate preferences play out? It’s hard to say.

If hiring managers want to have access to the widest possible talent pool, they should push for flexible working policies. On the other hand, if candidates are prioritising their career trajectory, considering full onsite working will open up more opportunities.

Get salary levels right, first time

With IRB Modeller salaries averaging around £60,000 – £90,000 depending on location / seniority / years of experience, businesses need to bear this in mind and offer competitive remuneration packages to attract and retain talent.

Regulatory modellers are in demand, meaning the candidate experience they have through your hiring process will contribute to their decision-making and whether to choose you over a competitor.

That’s why it’s vital to avoid low offers and commit to good salary levels that demonstrate positive company culture. Trying to save a couple of £££ could reflect badly on your business and result in losing out on your ideal candidate if they feel undervalued. It can even cost you more in the long run if you then have to start the process all over again!

Nuhaa draws on her experience to share some advice,

“It can be frustrating for everyone involved when a great candidate aces all the interviews, is really bought in to the company and opportunity, only for a low offer to fall flat and undermine the whole process. Always offer a candidate what they’re truly worth and, if you’re not sure, ask us! Yes, we can advise on market rates, but we’ve also built a relationship with the candidate, so we know what motivates them and how receptive they’ll be to different offers.”

Listen to the market

“Back in my day, we worked 70-hour weeks, were in the office full time, and didn’t need a pat on the back to know we were doing a good job.”

Times have changed. In the UK, working 50-60 hours was the average in 1870. It was also common to work 6-day weeks. A myriad of historical events between then and now mean that societal norms have evolved and those setups no longer make sense.

Whatever you put it down to – more females in the workforce, more dual income households, people retiring later, more value being placed on personal and family time – today’s workforce is living in very different circumstances and their priorities reflect that.

The only way businesses will be able to successfully recruit and, more importantly, retain talent is to adapt and embrace these changes.

With the shortage of skilled workers, and that being no secret amongst the candidate pool, they are in the driving seat. Employers need to be receptive to changing jobseeker priorities, new policies, and working setups. Under-offering or demanding five days in the office will get you nowhere in the long run.

With over 15 years under his belt leading credit risk teams and guiding FS businesses through significant change, Marcin Lomot shared his advice when it comes to regulatory modelling recruitment,

“The talent crunch will be quite inevitable as modelling of regulatory outcomes requires a wide range of both knowledge and skills, from the intimate understanding of a particular branch of regulation, ability (or courage?) to interpret policies and/or consultative papers, appropriate engagement with the regulator; through equally intimate understanding of the business’ strategy to, last but not least, ability to crunch numbers and turn them into an impactful story that would make the senior management interested and board members take note.

Whilst AI may eventually get there, firms that act fast to secure regulatory modelling talent displaying that fairly unique blend of skills early will most likely give themselves advantage over peers and potentially save on costs associated with navigating the impending regulatory changes in a compliant but also strategically relevant and financially optimised manner.”

3.2: Advice for Candidates (6 min)

On the Other Hand: The Candidate’s Perspective

While the demand for regulatory modellers in the UK is undeniably high, professionals in this field are not immune to the challenges of navigating the job market. Many experienced candidates find themselves facing hurdles in securing new roles, often feeling overlooked despite possessing the sought-after skills and knowledge.

Let’s delve into some of the key challenges regulatory modelling professionals are encountering:

Drowning in a Sea of Applications:

The very high demand for regulatory modellers can paradoxically create a bottleneck for candidates. Job advertisements often attract a significant volume of applications, many of which may not be a strong match for the role. This sheer number can mean even highly relevant CVs get lost in the initial screening process, making it difficult to stand out.

The “Relevance” Filter:

Despite possessing the core skills and experience, candidates may be overlooked if their CV doesn’t explicitly highlight the specific requirements (such as regulatory frameworks or modelling techniques) mentioned in the job description. Recruiters and hiring managers often rely on keyword searches and, in some cases, automated systems to sift through applications, meaning that even subtle differences in terminology can lead to a CV being disregarded.

The “Overqualified” Conundrum:

Some experienced professionals encounter the frustrating feedback of being “too experienced”. Hiring managers might perceive them as potentially being less engaged with the role in the long term, viewing it as a temporary stepping stone, or having salary expectations beyond the budget. This can be particularly disheartening for seasoned modellers seeking new challenges or a change of environment.

Application Fatigue:

The time-consuming nature of tailoring applications to each specific role and the often-limited feedback can lead to candidates feeling like they’ve “applied for everything already” with little success. This can be demotivating and create a sense of stagnation in their job search.

Why do these challenges exist?

Several factors contribute to these difficulties faced by regulatory modelling candidates:

High Application Volumes:

The increasingly widespread use of technology and AI-powered tools has made it much easier for candidates to fire out numerous job applications with minimal effort. This has led to a surge in applications, often from individuals who don’t wholly match the requirements, and ultimately floods hiring managers’ inboxes which makes it harder for truly qualified candidates to be seen.

Focus on Specificity:

The highly regulated nature of the financial services industry means employers often have very specific requirements regarding regulatory knowledge and modelling experience. If a candidate’s CV doesn’t immediately and clearly demonstrate these specific skills, they risk being overlooked.

Risk-Averse Hiring:

Given the critical nature of regulatory modelling, companies tend to be risk-averse in their hiring decisions. They often prioritise candidates with a proven track record in very similar roles and may be hesitant to take a chance on individuals whose experience, while relevant, isn’t an exact match.

Time Constraints on Hiring Managers:

Hiring managers are often juggling multiple responsibilities and may lack the time to thoroughly review every application, leading to a reliance on quick screening methods.

Advice for Regulatory Modelling Candidates to Overcome These Challenges

Despite these hurdles, regulatory modelling professionals can take proactive steps to improve their chances of securing their desired roles:

Don’t Be Deterred by Numbers – If You Fit, Apply!

Seeing a high application count on a job advert shouldn’t put you off if you genuinely meet the requirements. The reality is that a significant proportion of those applications are often unsuitable. By possessing the right experience and putting your hat in the ring, you’re already likely to be ahead of the curve in a sea of less relevant submissions, particularly given how easily candidates can now fire off applications thanks to technology and AI.

Nuhaa shares a recent experience which solidifies this point,

“We recently advertised a Lead Credit Risk Analyst role on LinkedIn. Within a matter of days, it had received over 640 applications. Of those, around 1 in 5 had the ‘must-have’ experience, and of course that gets whittled down further as we screen and dive deeper into people’s skills. If you know you fit the bill, don’t be deterred by high application numbers – you’ll stand out as one of the few who actually meets the requirements.”

Tailor Your Application Meticulously:

Don’t fall into the trap of sending out generic CVs. Carefully analyse each job description, identify the key regulatory frameworks, modelling techniques, and required experience, and ensure these are prominently featured in your CV, particularly in a concise professional summary at the top. Use the exact terminology used in the job advert where applicable.

See also: 5 Tips for Writing a Job-Winning CV (using AI) >

Make Relevance Unmissable:

Imagine the hiring manager has only a few seconds to scan your CV. Ensure your most relevant experience, skills, and qualifications are immediately visible on the first page. Don’t make them search for it. Use clear headings and bullet points to highlight your key achievements and responsibilities related to regulatory modelling.

Ellie has spoken to many candidates in her 20 years of recruiting, and the feeling of being suitable for the job but still overlooked is a persistent challenge,

“One of the biggest frustrations for candidates is being relevant but not getting noticed. Often, this comes down to the content on the CV. We always advise candidates to really tailor their CV to each specific role, explicitly drawing out the connections between their experience and the employer’s needs. If you have the skills, spell it out – don’t assume a hiring manager will ‘read between the lines’.”

Address the “Too Experienced” Concern Proactively:

If you anticipate this feedback, consider addressing it in your covering letter or during an initial conversation. Clearly articulate your motivations for applying for the specific role, emphasising your genuine interest in the opportunity and how your extensive experience can bring significant value to the team. Highlight your adaptability and willingness to contribute at all levels.

Take a Direct Approach (Strategically):

If you’ve applied for a role, you’re confident you’re a strong fit but haven’t heard back, consider a targeted outreach on LinkedIn. Find the recruiter or hiring manager and send a brief, personalised message reiterating your key qualifications and expressing your strong interest. This can help your application stand out from the general influx.

Leverage the Power of Recruiters:

Specialist recruitment agencies focusing on financial services and risk management (like MERJE!) have in-depth knowledge of the market and established relationships with hiring managers. Reach out to these recruiters, share your career goals and experience, and let us work on your behalf.

We can provide valuable insights into available opportunities, such as greater detail about the business, team, interview process, interviewers, and how to pitch yourself. We can also advocate for your candidacy – after all, your success is in our best interest.

We will also pick up the phone whenever we hear about a new or upcoming vacancy that fits your skills, reducing the work you have to do in searching for adverts to apply to.

Network Actively:

Don’t underestimate the power of your professional network. Inform your contacts about your job search and ask if they are aware of any relevant openings within their organisations. A personal referral can significantly boost your application’s visibility.

Be Proactive and Persistent:

Don’t solely rely on job boards. Research companies you are interested in and explore their careers pages directly. Even if there isn’t a suitable vacancy advertised, consider reaching out to their recruitment team or relevant department with a compelling introduction and your CV. Often, success on this front will come down to timing. They may have a job coming up or will at least have you top of mind when something does arise.

Refine Your Online Presence:

Ensure your LinkedIn profile is up-to-date and reflects your skills and experience accurately. Many recruiters and hiring managers use LinkedIn to source candidates and verify information.

See also: 7 Tips to Optimise Your LinkedIn Profile >

By understanding the challenges and adopting a strategic and proactive approach, regulatory modelling professionals can significantly improve their chances of securing their next career step.

Related Articles:

Section 4: Future Trends & Predictions (1 min)

Looking ahead at the changing shape of financial regulation and its potential impact on modelling techniques and required skills.

What does the future of financial services look like? And how will that impact the demand for credit risk professionals and regulatory modellers?

With another AI-powered solution popping up every few minutes, new generations of consumers revolutionising what we understand about customer desires, and wider, global issues like climate change, economy fluctuations, and political shifts, it’s tough to predict exactly what the next decade holds for the UK financial services industry.

The UK government has emphasised the need to increase growth and competitiveness within the financial services sector, and aims to do so with its Financial Services Growth & Competitiveness Strategy. This includes a focus on attracting global investment, supporting the adoption of new technologies like AI and digital assets, and streamlining the regulatory framework.

Let’s look at what Ellie and Nuhaa think might be in store for financial services over the coming years…

4.1: AI in Financial Services (6 min)

AI is rapidly transforming the financial services industry in the UK. Businesses are increasingly leveraging AI for a variety of applications and, in credit risk in particular, AI is being used to improve predictive analytics, automate decision-making, and enhance risk assessment.

A Bank of England report found that 75% of firms are already using artificial intelligence (AI), with a further 10% planning to use AI over the next three years.

While the adoption of AI in financial services is not fully established just yet, it is already having a significant impact and is by no means slowing down.

In fact, Accenture modelling has shown that some FS sub-sectors will see substantial productivity gains in the next 15 years thanks to generative AI. They predict over 30% gains for capital markets, banking, and insurance, with potential cost savings of £9.7 billion, £12.7 billion, and £3.4 billion respectively.

Accenture’s research also indicates that Generative AI could potentially automate or augment up to 45% of current financial services work activities.

What might that look like for credit risk modellers?

Ellie predicts a drastic change in the skillsets we expect from credit risk and regulatory modelling professionals:

“AI will undoubtedly drive a shift in the skills practised by credit risk professionals. While traditional modelling skills will remain important, there will be an increased demand for expertise in areas such as machine learning, data science, and AI ethics.”

It’s true – with AI likely to automate some of the more routine tasks performed by credit risk modellers, such as data cleansing and transformation, summarising key insights, compiling reports, and trend spotting, this will free up time to focus on higher-level responsibilities. The credit risk skillset will therefore transition towards business activities that AI cannot (or should not) do, for example:

- Developing new modelling techniques

- Validating complex AI models

- Considering wider business and commercial impacts

- Translating data and predictions into ingestible, actionable insights for a variety of stakeholder audiences

- Ensuring AI is used in a fair and unbiased manner

- Understanding the realistic capabilities and limits of AI

- Managing and monitoring the embedding of AI throughout the credit risk life cycle

- Strategic decision making on process optimisation, approach and methodology choice, operational enhancement, etc.

Discussing the impact of AI on regulatory modelling resource needs, Jamie Hopkins adds,

“Whilst modelling skills are still in demand, the use of AI in the regulatory modelling space is still being determined with no clear roadmap. However, AI will inevitably lead to less resource requirements. While the use of AI is still being established, the skills and experience that employers look for in regulatory modellers will change as AI becomes more integrated in modelling teams.”

The dangers of skill atrophy

The increasing reliance on AI also brings the risk of skill atrophy. It’s crucial to strike a balance; as credit risk professionals adopt AI more for day-to-day activities, there’s a danger you may practise your core skills less and ultimately lose them. You must use AI to support your work, without becoming overly dependent and losing your ability to perform essential tasks independently.

Nuhaa shares her advice for credit risk professionals in the wake of AI adoption and advancement,

“I would advise credit risk professionals to continue honing core skills while broadening their expertise into areas AI can’t address. Developing strong communication skills is also essential, not just for explaining complex AI concepts to those without a technical background, but the nuances of real human-to-human conversations are likely something that AI will never be able to fully replicate, so having adaptable communication abilities, influencing, and relationship building skills will make you indispensable as AI automates the BAU tasks.”

What else might change with AI?

The advancement of AI is poised to bring about significant changes across financial services, from regulations and skills demand to products, their availability, and the processes behind them.

Credit assessments:

Predictive analytics, driven by AI, is fundamentally changing how financial institutions assess risk, detect fraud, and personalise services, moving beyond traditional reliance on historical credit data and financial statements.

AI-driven models use machine learning to dynamically assess creditworthiness, incorporating real-time and behavioural data for more accurate and fairer lending decisions. This approach, by integrating predictive analytics with alternative data sources like transactional bank data and open banking initiatives, enables financial institutions to expand credit access while mitigating default risks, creating opportunities for previously underserved individuals and businesses.

Looking ahead, the integration of AI in credit assessments is poised for significant advancement. We can expect to see more Explainable AI techniques being developed to address the black-box problem, providing greater transparency into how AI models arrive at their decisions. This will be crucial for building trust with both consumers and regulators.

It’s also possible, though will come with its own objections and challenges, for wider alternative data sources, such as social media activity and utility payment history, to be used to provide a more holistic view of creditworthiness.

As well as this, advancements in natural language processing (NLP) will also enable lenders to extract valuable insights from unstructured data, such as loan applications and customer correspondence.

Scenario modelling, predictions, and market shifts:

AI-driven predictive analytics is enabling more robust and comprehensive stress testing, scenario modelling, and rapid shifts in response to extreme market disruptions.

With the ability to incorporate layered models, real-time data processing, adaptive machine learning techniques, and alternative data sources like sentiment analysis, macroeconomic indicators, supply chain disruptions, and consumer spending patterns, institutions can maintain financial stability, optimise risk strategies, and make more informed decisions in volatile markets.

As AI technology progresses, it will be possible to create models which can process and analyse even larger and more complex datasets in real-time. The integration of quantum computing and AI could further enhance predictive capabilities, allowing for the simulation of complex scenarios that are currently beyond our computational reach.

Regulations:

As AI becomes more integrated into financial systems, regulators will face the challenge of developing frameworks that promote innovation while mitigating potential risks. This is a complex area, with concerns around:

- Data Protection and Privacy: AI models rely on vast amounts of data, raising concerns about how this data is collected, stored, and used, and the potential for breaches of data protection regulations.

- Ethics: The use of AI in credit risk can raise ethical dilemmas, such as the potential for algorithmic bias, which could lead to unfair or discriminatory outcomes for certain groups of borrowers.

- Transparency and Explainability: Some AI models, particularly deep learning models, are often “black boxes”, making it difficult to understand how they arrive at their decisions. This lack of transparency can be a major concern for regulators.

- Accountability: Determining who is responsible when an AI model makes an error or causes harm is a significant challenge.

To address these concerns, regulators are beginning to develop specific AI regulations. For example, the European Union’s proposed legal framework for AI classifies Generative AI models into various risk-based categories.

This framework establishes a risk-based approach, where the level of regulation depends on the potential impact of the AI system on human health, safety, and fundamental rights. The framework also introduces sanctions and remedies for non-compliance, as well as a system of monitoring and enforcement. It is likely that the UK will follow suit with similar regulations.

Jamie Hopkins shared some insight on upcoming AI regulations,

“The PRA released a discussion paper DP5/22 back in October 2022, and recently formed an AI Consortium in Sept 2024 to debate the use of AI in Financial Services. So, I expect the PRA to announce regulation around the use of AI sooner rather than later (especially on the back of the EU AI Act 2024).”

Business Operations:

Businesses that effectively adopt AI can gain a competitive edge through increased efficiency, improved accuracy, faster decision-making, enhanced risk management, reduced costs, and greater scalability.

However, they also face potential risks.

Costly errors and severe consequences can come from models which are inadequate, flawed, biased / discriminatory, or unreliable. These issues can come from inaccurate or incomplete data, over-reliance on AI without the proper checks, or falling behind when it comes to emerging AI regulations and compliance.

Additionally, implementing and embedding AI within existing processes and technology can require significant time and monetary investment. Doing this without thorough planning and a strategic thought process will be incredibly costly.

Ellie adds,

“Investing in AI technology without a clear understanding of its intended use, the specific problems it’s meant to solve, and how it aligns with overall business objectives can lead to wasted resources. The initial investment, ongoing maintenance, and the cost of hiring specialised personnel can strain budgets if the AI implementation doesn’t deliver the expected returns or if the technology becomes obsolete before providing adequate value.”

4.2: Climate Risk (3 min)

As the effects of climate change are more heavily felt far and wide, the importance of integrating climate risk across other areas of risk management is becoming more obvious.

In short, climate change presents a significant threat to financial stability and its impact, primarily felt through physical risks (climate-related events like extreme weather) and transition risks (resulting from the shift to a low-carbon economy). This means regulators are pushing for the integration of climate risk into credit risk models to ensure that banks and other lenders adequately account for potential losses.

This is being carried out in a variety of ways: climate-related scenario analysis and stress testing, incorporating climate risk factors and variables in PD, EAD, and LGD parameters, and factoring climate risk scores in credit assessments.

Despite the progress made, integrating climate risk into credit risk models remains challenging, with hurdles such as data availability and quality, model complexity, and vast uncertainty when it comes to predicting the scope and impact of climate change.

Looking ahead, we can expect to see:

Improved Data and Tools: Efforts to improve the availability and quality of climate data, as well as the development of more sophisticated tools for assessing climate risk.

Greater Regulatory Guidance: Regulators will provide more specific guidance on how financial institutions should integrate climate risk into their risk management frameworks.

Increased Collaboration: Collaboration between financial institutions, researchers, and policymakers will be essential to advance the understanding and management of climate-related financial risks.

For credit risk and regulatory modelling professionals, this means…

Greater demand for new and existing skills:

- Climate Science Literacy: Understanding the fundamentals of climate science, including the causes and consequences of climate change, and how it translates into financial risks.

- Climate Risk Modelling Expertise: Proficiency in using and developing models that can assess the impact of climate change on credit risk, including scenario analysis, stress testing, and econometric modelling.

- Data Analysis and Management: The ability to source, analyse, and manage large datasets, including climate data, and integrate them with financial data.

- Regulatory Knowledge: Keeping abreast of the regulatory landscape related to climate risk, including disclosure requirements, stress testing guidelines, and capital adequacy rules.

- Interdisciplinary Collaboration: The ability to work effectively with climate scientists, economists, and other experts to incorporate climate risk into financial models.

And evolving and novel job titles and responsibilities:

- Climate Risk Analysts/Managers: Professionals who specialise in assessing and managing climate-related financial risks within financial institutions.

- Climate Risk Modellers: Experts who develop and implement the quantitative models used to assess climate risk.

- Regulatory Reporting Specialists: Professionals who focus on ensuring that financial institutions comply with climate-related reporting requirements.

- ESG (Environmental, Social, and Governance) Risk Specialists: Professionals who assess and manage the broader range of ESG risks, including climate risk, and their impact on financial institutions.

Anil Somani, Credit Risk Modelling Manager who has recently turned his credit risk modelling skills to the area of climate risk, shares his experience,

“I believe the recent CP10/25 and evolving expectations from the PRA on climate related risk management will result in an increase in demand for regulatory modellers within credit risk.

Credit risk professionals need to be aware of the physical and transition climate risks that can impact their portfolios from a PD and LGD perspective, and also be able to monitor their exposure to climate risks such as flood risk and EPC distributions on an ongoing basis via credit risk MI and risk appetite metrics.

From my personal experience, I had been a stress testing modeller for a number of years with experience in IFRS9 and IRB and have now upskilled into Climate Risk modelling. It makes sense for firms to upskill existing modellers given the transferable skills, and the modelling techniques for climate scenario analysis modelling is similar to stress testing modelling.”

Ultimately, those who can effectively bridge the gap between climate science and finance will be in high demand, driving the development of new expertise and career paths in the financial services industry.

4.3: Emerging FS Products & Services (4 min)

Another reason why financial services regulations are now more plentiful, complicated, and in the public eye in recent times is the emergence of new products and services.

As consumer preferences change, the financial services world responds. With that, the last few years have seen the growth of Buy Now, Pay Later (BNPL), Crypto-Assets, and more.

These emerging financial services and products often fall outside the scope of existing regulations, necessitating the development of new rules or the adaptation of existing ones.

It’s no wonder, then, that banks, building societies, fintechs, insurance providers, and other financial institutions have ramped up their hiring efforts when it comes to analysts, modellers, and leaders with regulatory expertise.

Here’s a look at some of these innovations and their regulatory implications in the UK:

Buy Now, Pay Later (BNPL):

BNPL has surged in popularity, offering consumers a way to spread the cost of purchases. However, concerns about unregulated lending, consumer over-indebtedness, and inconsistent credit checks have led to calls for greater regulatory oversight.

The future of BNPL likely involves increased regulation to protect consumers, standardised credit checks, and ensuring responsible lending practices. We might also see greater integration of BNPL services into mainstream finance, with partnerships between BNPL providers and traditional banks.

Crypto-assets:

Crypto-assets like Bitcoin and Ethereum have gained prominence, but their volatility, lack of transparency, and potential for use in illicit activities pose regulatory challenges. The UK is working to establish a regulatory framework for crypto-assets, balancing innovation with consumer protection and financial stability.

The future of crypto-assets hinges on regulatory clarity, technological advancements and wider adoption by individuals and institutions. We could see increased use of crypto-assets for payments, investment, and other financial applications, as well as the development of new types of crypto-assets.

Decentralised Finance (DeFi):

DeFi aims to create a financial system without traditional intermediaries, using blockchain technology. While DeFi offers potential benefits such as increased efficiency and accessibility, it also presents risks related to security, smart contract vulnerabilities, and regulatory arbitrage.

DeFi has the potential to disrupt traditional finance by offering more transparent, efficient, and accessible services. However, its future depends on addressing security concerns, improving scalability, and developing robust regulatory frameworks.

Neobanks:

Digital-only banks like Monzo and Starling, operating without traditional branch networks, have grown significantly in the past few years. They cater to a new generation of tech-savvy consumers by offering innovative features, lower fees, and a user-friendly experience.

Neobanks are expected to continue growing, driven by increasing demand for digital banking solutions. There is no doubt that they will look to leverage AI to enhance the customer experience, but this must be done with caution to ensure regulatory compliance and data privacy. Many neobanks also boast strong ESG values, so the environmental impacts of AI must be taken into account.

Embedded Finance:

Integrating financial services into non-financial platforms, like offering payment solutions or lending options within e-commerce platforms, is a growing trend. While this raises questions about regulatory responsibilities, data sharing, and consumer protection, its potential has been a major driver of consistently high fintech investment levels. In fact, McKinsey has estimated that European embedded finance could account for revenues of over $104 billion by the end of the decade.

We can expect to see more non-financial companies offering financial services seamlessly within their platforms, creating new revenue streams and enhancing customer loyalty. This trend could blur the lines between traditional financial services and other sectors.

Fintech Super Apps:

Fintech super apps are all-in-one platforms that offer a wide range of financial services, such as payments, banking, investments, and insurance, often combined with other services like e-commerce and social media.

The future of fintech super apps points towards further expansion and integration of services, potentially creating dominant platforms that cater to a wide range of user needs. This could lead to increased competition among financial institutions and tech companies, as well as new regulatory challenges related to data privacy, market concentration, and systemic risk.

The Need for New and Adapted Regulations

In the wake of the rapidly shifting societal preferences that come with technological advancement and new generations, financial services providers are responding with novel and innovative solutions. As such, regulators face the challenge of:

- Balancing innovation and risk

- Keeping pace with technological change

- Addressing cross-border issues

- Protecting consumers

Ultimately, the emergence of new financial services and products is driving significant changes in the regulatory landscape, increasing the demand for skilled regulatory modellers who can help navigate this complex and evolving environment.

Nuhaa adds,

“Those professionals who keep abreast of the latest technology, regulations, and wider consumer trends will be most sought after by FS businesses looking to keep up with, if not lead, the market.”

Ellie, Nuhaa and our guest contributors’ insights underscore a crucial constant in the ever-changing UK financial services landscape: the enduring demand for robust regulatory modelling. Far from a fleeting trend, this skillset is a fundamental requirement in the wake of increasingly complex regulations, economic pressures, and rapid technological advancements.

Regulatory modelling has solidified its position as a vital discipline, consistently sought after by UK financial institutions to manage compliance and risk. While the tools and techniques of the trade will undoubtedly evolve – with AI poised to revolutionise data analysis and automation – the core need for professionals adept at interpreting and implementing regulatory frameworks through quantitative methods will only intensify.

The future of UK financial services, characterised by its ongoing intricacy and innovation, will continue to rely heavily on these skilled individuals to ensure stability, protect consumers, and drive healthy market growth.

Many thanks to the collaborators and contributors involved in this report:

Anil Somani – Credit Risk Modelling Manager

Jamie Hopkins – Senior Credit Risk Contractor

Marcin Lomot – Credit Risk & Regulatory Expert